A refinance is typically taken out on a property after it has gone through some improvements or to extract equity out of a project after some amount of time. It is common for a refinance to be used to repay an acquisition loan or a construction loan.

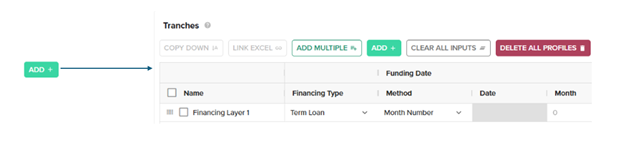

1. Open the U-Rite calculation engine and navigate to the “Financing” tab in “Property Inputs”

2. Click the “ADD +” button – this will place a template loan in the row area

3. A refinance will be a “Term Loan” so you can keep the financing type the same.

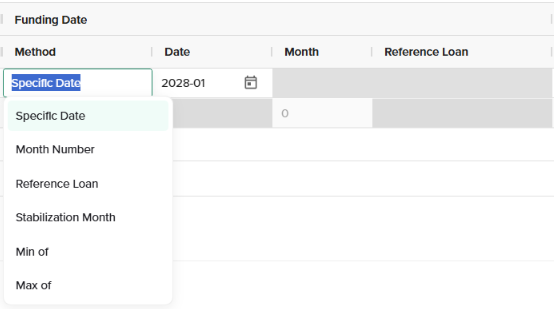

In the funding date area – enter the funding date there are several methods we can choose like specific date, month number stabilization date, or reference loan.

Specific date – Will disperse on the month given. The entry 2028-01 will disperse the funds for this loan January 2028.

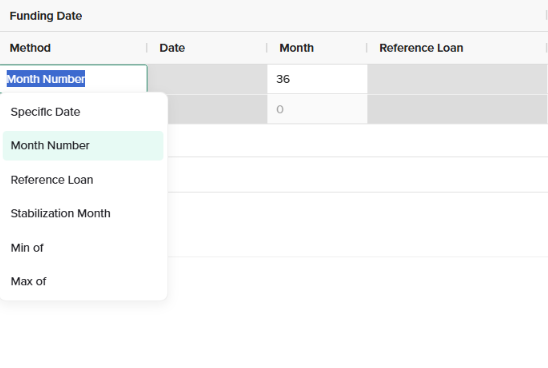

Month Number – Will disperse the loan this many months after the analysis start date – for instance if the start date is 2026-01-01 and the month number is 36,the loan will disperse on 2029-01-01.

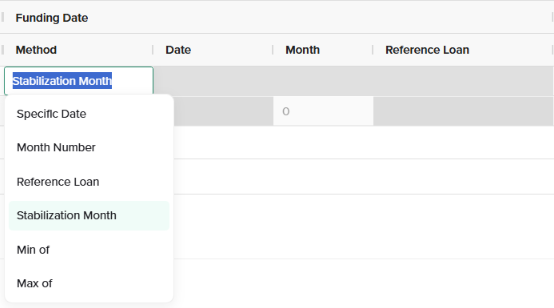

Stabilization date – Will disperse on the month designated the stabilization month – this can be entered in the “Analysis Settings” Input tab. If the stabilization month is when the building is 100% occupied then there finance will take place in that month.

Reference Loan – Will disperse the same month the referenced loan is repaid.

4. Choose a loan Amount Method and a Loan amount

Amount – Fixed dollar amount that will be dispersed.

Loan-to-value % - will disperse a % of the value of the building – either a %of the purchase price or a percentage of the value of the building based on a cap rate.

Min DSCR – Will disperse a loan where NOI is equal to this multiple of the debt service amount.

Min Debt Yield – Will disperse a loan so that the NOI divided by the loan amount is equal to the amount entered.

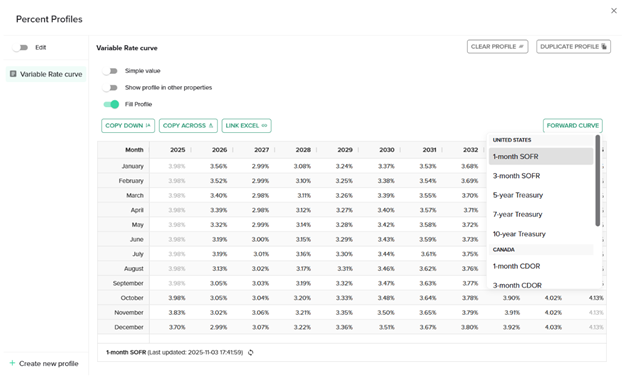

5. Enter in the interest rate – we have the option of base rate and spread – in the base rate area you can create a profile with varying rates or use one of our preset variable rate profiles like 3-Month SOFR. The spread will then be applied on top of the base rate and that combined figure will be the nominal annual rate for a month. For instance if a month has an interest rate of 3% and a spread of 3% that month’s Nominal annual rate will be 6% so the monthly interest rate will be 0.5%.

6. Enter in other standard loan inputs like Term, Amortization, I/O Period, Financing Fees in their appropriate input cells.

The loan will appear in the cash flow model in the section directly beneath the unlevered cash flow.